OP ED #3 CRITICAL MINERALS | Eight key critical minerals projects in Australia’s $10bn pipeline

Sign up for updates

Sign up to receive occasional updates on major climate and energy finance news and developments, and notification of new reports, presentations and resources.

"*" indicates required fields

Read our privacy statement here.

OP ED #3 CRITICAL MINERALS | Eight key critical minerals projects in Australia’s $10bn pipeline

By Tim Buckley and Matt Pollard, CEF.

Australia has the potential to be a Critical Minerals Mining and Refining Superpower, providing world-scale secure supply of critical inputs to the global energy transition. Many refining projects are very energy intensive, providing a further opportunity for Australia to accelerate global decarbonisation by leveraging our vast, largely untapped low-cost renewable energy resources to power onshore refining and value-add pre-export.

In 2021 Climate Energy Finance provided expert advice into the BCA / ACTU / ACF / WWF‘s Accenture report “Sunshot: Australia’s opportunity to create 395,000 clean export jobs”.[1] At the time, “clean exports” was a largely hypothetical exercise; the investment flows had yet to materialise, and our then-government refused to even accept the climate science, let alone the inevitability of the energy transition, including the global pivot to electric vehicles (EVs) – essentially batteries on wheels, requiring a massive upscaling in mining and refining of lithium. A year later global EV sales are on track to double to over 10m in 2022, we have the Climate Change Bill 2022 and Australia has now exported its first shipment of battery grade, refined lithium hydroxide (LHM), the precursor for battery cathodes.

This is just one example of the accelerating momentum behind this shift. Capital flows are accelerating. We have identified over $10bn of investment proposals in resource value-adding across Australia. Several are in production already and a number have moved beyond final investment decision (FID) and are under construction.

In this note we review eight value-adding refining projects in lithium, rare earths, nickel, copper, green zinc and premium, high iron content iron ore for high-efficiency steelmaking.

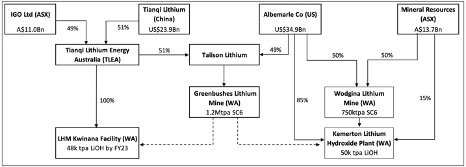

1.Tianqi Lithium (China) & IGO Ltd LHM Refinery, Kwinana, WA

The first of two trains at Australia’s first LHM plant was commissioned in May 2022 at Kwinana, WA by Tianqi Lithium Energy Australia (TLEA), a joint venture between Tianqi (51%) and ASX-listed IGO (49%). Train I is in commissioning and Train II in construction (commissioning due 2024),[2] with planned further investments into Train III and Train IV. Each train will have the capacity to produce 24,000 tonnes pa (24ktpa) LHM. Total potential capacity of I-IV is planned at 96ktpa LHM.[3] Spodumene concentrate (high purity lithium ore) throughput is being obtained from the Greenbushes lithium mine, which is a joint venture between TLEA (51%) and Albermarle (49%).

2. Albermarle Co (US) & Mineral Resources LHM Refinery, Kemerton, WA

A two-train LHM plant at Kemerton, WA saw Train I commissioned in July 2022. First product from Train II is expected 2QFY2023, taking the capacity to 50ktpa. This refinery is owned by a joint venture of Albermarle (60%, going to 85%) and ASX-listed Mineral Resources (40%, going to 15%).[4] Spodumene concentrate is being obtained from the Greenbushes mine.

Figure 1: Lithium Mining and Refining, WA (IGO, Mineral Resources, Tianqi & Albermarle)

Source: Company Accounts, Climate Energy Finance calculations

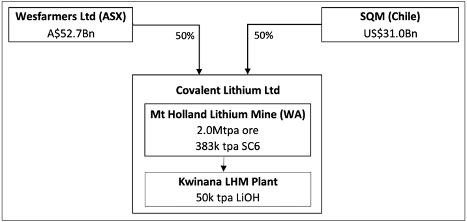

3. SQM (Chile) & Wesfarmers LHM Refinery, Kwinana, WA

A third 50ktpa LHM plant is due to be commissioned at Kwinana by the end of 2024 by Covalent Lithium, a joint venture between Sociedad Química y Minera de Chile S.A. (SQM) and ASX-listed Wesfarmers Limited – Figure 2. Covalent also operates the Mount Holland lithium mine, which will supply the Kwinana refinery.

Figure 2: Lithium Mining and Refining, WA (Wesfarmers & SQM)

Source: Company Accounts, Climate Energy Finance calculations

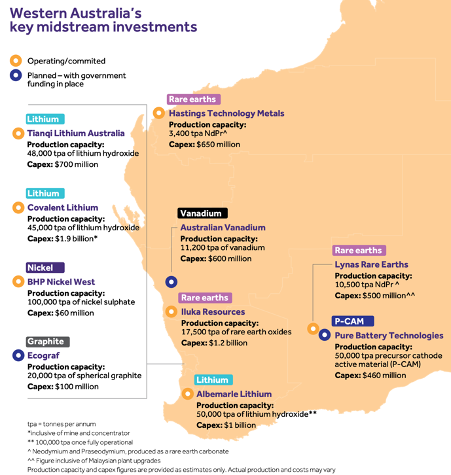

4. Lynas Rare Earths processing facility, Kalgoorlie, WA

ASX-listed Lynas Rare Earths is the world’s only significant producer of separated rare earths outside of China, and is planning significant mine capacity expansions. May 2022 saw Lynas start construction of a new rare earths processing facility in Kalgoorlie to value-add onshore its Mount Weld mine, with a project cost of $500m (including associated upgrades at the Lynas Malaysia plant). Once operational, mixed rare earths carbonate will be shipped directly from Kalgoorlie to the Lynas plant in Malaysia for further processing, or to Lynas’ proposed US Rare Earths Separation Facility. The Kalgoorlie plant has been designed to facilitate processing of third-party rare earths concentrate from other Australian projects as they come online, and will create 209 positions during construction and 128 new ongoing jobs.[5] [6][MP1]

In April 2022, ASX-listed Iluka Resources announced it had reached FID on the development of Australia’s first fully integrated 17,500tpa rare earths refinery at Eneabba, WA with a capex of over A$1.2bn.[7] This will be covered in a subsequent review.

5. BHP’s Nickel West Smelter Upgrade, Kwinana, WA

Underlying its divestment of its petroleum business to Woodside, BHP has progressively pivoted its corporate strategy to “secure further growth opportunities in future facing commodities” essential to the energy transition and economic growth, with BHP CEO Mike Henry noting that, “The world will need more copper and nickel for electrification, renewable power and electric vehicles.”[8] BHP’s 2022 asset split is 50% copper/nickel, 31% iron ore, 14% coal and 7% potash (although the profit spilt is 52% iron ore weighted, reflective of this division’s exceptional profitability).[9]

At the end of 2021 BHP finished a $60m 100,000tpa nickel sulphate refinery at Kwinana, WA as an Australian-first.[10] BHP reports every EV battery requires 40kg of nickel and that 90% of its nickel goes into the global battery market. It expects demand for nickel in batteries to increase by 500% in the next decade. BHP’s Nickel West employs over 2,500 people and its operations include a fully integrated mine-to-metal business. Three mines at Mt Keith, Leinster and Kambalda have concentrator plants to process ore. The three streams feed into the Kalgoorlie nickel smelter, which uses a flash furnace to convert the nickel into nickel metal in the form of powder and briquettes, and then to a high purity battery-grade nickel sulphate plant, also in Kwinana. The nickel sulphate plant created 80 new direct jobs, in addition to the 200 jobs created during construction phase.[11]

6. BHP’s Bid for Oz Minerals

In August 2022, BHP made a $25ps, A$8.4bn bid for Oz Minerals, but this was rejected by the board, with recent speculation that BHP will return with a higher offer.[12] The key assets of Oz Minerals are copper and nickel mines and resources in South Australia, providing synergies with BHP’s copper-gold-silver-uranium operations around Olympic Dam, and the optimisation of the existing copper smelter and refinery. BHP is looking to leverage scale of the combined mine-to-refinery business, underpinning new potential initiatives of building a desalination plant and a $500m, 320MW renewable energy power purchasing agreement (PPA) signed in October 2021 with Iberdrola to reduce the mine emissions from electricity consumption by 50% by 2025, creating 200 construction jobs.[13] Oz Minerals brings significant new mine capacity potential, including the newly approved $1.7 billion copper-nickel West Musgrave mine in remote Western Australia, bringing 1,500 new construction jobs.[14]

7. Sun Metals Green Zinc, Townsville, North Queensland

Korea Zinc’s Sun Metals in Townsville is well on track to be one of the world’s first fully green zinc refineries. Employing 350 staff, the company has committed to running this refinery on 100% renewable energy by 2025 as part of a global corporate goal of 80% renewables by 2030. In 2018 it invested $200m to build an adjacent 143MW solar farm that provides 25% of its electricity needs. Sun Metals has subsequently taken a one-third equity stake in the $2bn 1,026MW Macintyre wind precinct being built by Acciona Energia and supported by Queensland’s CleanCo.[15] This windfarm will provide another 64% of Sun Metals electricity needs. Sun Metals’ Ark Energy CEO Daniel Kim said, Macintyre will help decarbonise the zinc refinery, enabling it to become one of the first major refineries in the world to produce “green zinc”.[16] September 2022 saw Daniel Kim announce that strategic partnerships would be essential to building a 3GW of renewables plan as part of its proposed new green ammonia supply chain from Australia to Korea.[17]

8. Fortescue Metals Group’s Iron Bridge Iron Ore project in the Pilbara, WA

Fortescue is looking to commission in March 2023 stage 2 of its US$3.7bn (A$5bn) Iron Bridge magnetite mine-and-processing project 145km south of Port Hedland in the Pilbara.[18] Approved back in 2019,[19] there have been some covid-19 delays. The vast majority of Australia’s $100bn annual export of iron ore is haematite of 50-63% iron content. In contrast, the 22Mtpa Iron Bridge targets a 67% iron content, the equal highest premium product of all major mines globally, a critical pre-requisite to higher efficiency steel-making.

Fortescue has been very vocal about the enormous investment opportunities in decarbonisation, and has committed to a US$6.2bn investment program this decade to build out wind and solar infrastructure, and the associated battery firming capacity.[20] This also includes heavy equipment fleet electrification to remove the current reliance on imported diesel, along with the Pilbara Energy Connect, a US$700m grid transmission project to provide electricity links to a number of key Fortescue facilities in the Pilbara.

CEF sees value-adding Australian resources pre-export as a massive opportunity to leverage our world-leading renewable energy potential and assist global decarbonisation, given much of the world’s future facing minerals are currently processed in China by a coal-heavy electricity grid. While Fortescue’s existing iron ore exports are lower quality 50-60% iron content haematite mines (average FY2022 pricing was just 72% of the 62% CFR index), Fortescue has undertaken a significant US$3.7bn investment in value-adding at well-above-index price expectations for Iron Bridge. Adding zero emissions electricity capacity is an obvious next stage of value-adding / decarbonisation of this new mine.

Figure 3: West Australian Refining Opportunities

Source: Government of Western Australia, Battery and Critical Minerals Prospectus, June 2022

Australia critically needs to see a strategic public-private focus on the value-adding of our world leading renewable energy and critical mineral resources, so as to maximise the investment, regional employment and export value-adding opportunities for our country as we embrace the enormous opportunities of the global energy transition.

This analysis is for public interest purposes highlighting the national strategic interests and opportunities for Australia from the global energy transition. It should not be construed in any way as general nor specific financial advice. The authors own shares in BHP and Wesfarmers.

[1] Business Council of Australia, Sunshot: Australia’s opportunity to create 395,000 clean export jobs, 14 October 2021

[2] S&P Global, IGO, Tianqi successfully produce first LHM at Australia’s Kwinana refinery, 23 August 2022

[3] Kwinana Lithium Hydroxide Refinery Site Visit Presentation. (29 July 2022)

[4] Mineral Resources, FY2022 Full Year Results, 29 August 2022

[5] Lynas, Lynas announces A$500m Mt Weld Expansion, 3 August 2022

[6] Lynas, Kalgoorlie RE Processing Facility Project Fact Sheet.

[7] Iluka Resources, Eneabba Rare Earths Refinery FID, 3 April 2022

[8] BHP, Growing value and positioning for the future, 18 August 2021

[9] BHP 2022 financial results and operational reviews, 16 August 2022

[10] West Australia, A Global Battery and Critical Minerals Hub, June 2022

[11] BHP, BHP delivers first crystals from Kwinana nickel sulphate plant, 1 October 2021

[12] AFR, BHP Weighs Boosting $8.4b Bid for OZ Minerals, 17 September 2022

[13] Iberdrola, Iberdrola will supply green energy to the BHP Olympic Dam mine project in South Australia, 14 October 2021

[14] AFR, OZ Minerals gives green light to $1.7b copper-nickel mine, 23 September 2022

[15] AFR, Queensland wind to power Telstra under Korea Zinc deal, 4 October 2022

[16] Renew Economy, First concrete foundation poured in Australia’s first gigawatt scale wind project, 14 September 2022

[17] Renew Economy, Korea Zinc plans 3GW renewable hub in huge Queensland green hydrogen play, 21 September 2022

[18] FMG Investor Presentation – Pilbara Operations Site Tour, October 2022

[19] FMG Press Release, US$2.6 billion Iron Bridge Magnetite Project approved, 2 April 2019

[20] The Brisbane Times, Forrest ‘locked and loaded’ for net-zero but does Fortescue have the calibre?, 2 October 2022